Body

The last quarter of 2021 yielded mostly positive returns for equities and flat returns for fixed income securities. Markets were helped by delightful amounts of fiscal spending that contributed to an almost $1.2 trillion expansion in the U.S. public debt in the fourth quarter alone.1 This deficit spending was partially funded by the $309 billion expansion in the Federal Reserve’s balance sheet for the quarter and multiples of that for the year.2

Image

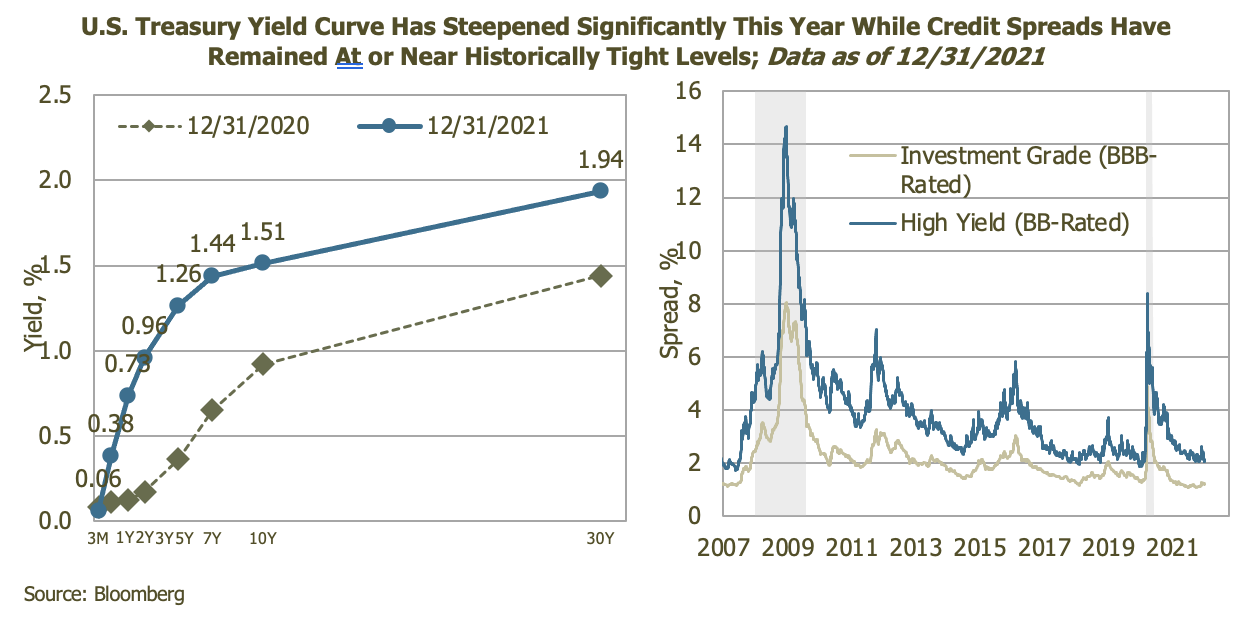

The last quarter of 2021 yielded mostly flat returns for fixed income securities. The Bloomberg U.S. Aggregate Bond Index’s flat return for the quarter kept year-to-date losses to 1.5%. This was the third-worst year since the index’s inception in 1975, with the worst year being 1994 when the index returned -2.9%. That year, the 10-year Treasury yield rose from 5.8% to 7.8%. In 2021, the 10-year Treasury yield rose from a paltry 0.93% to a slightly less paltry 1.52%.

Image

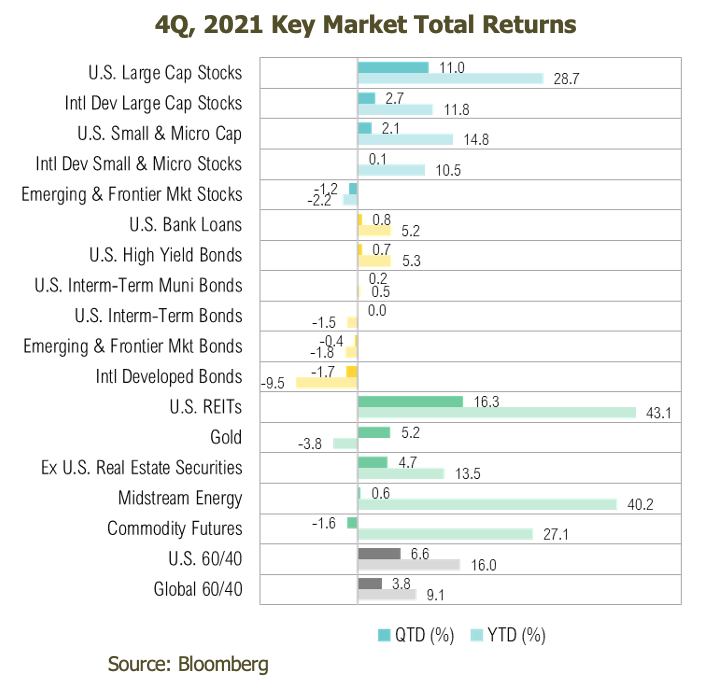

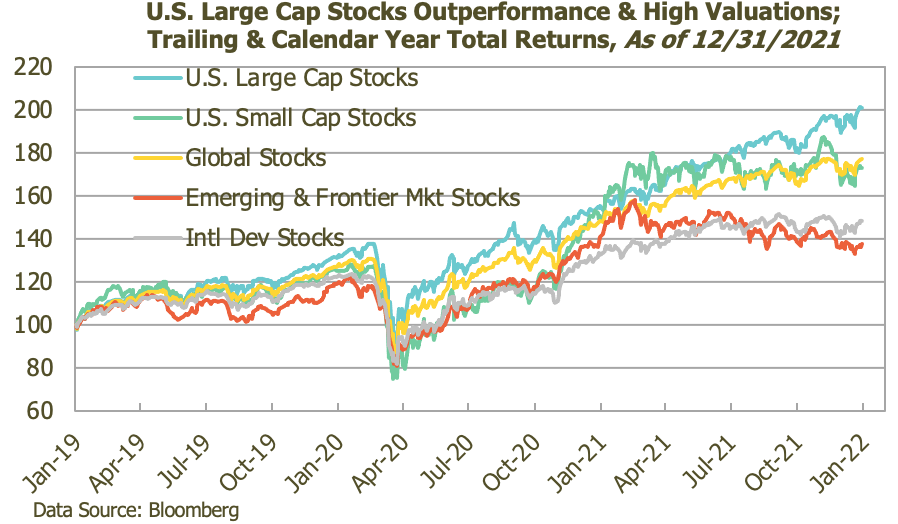

Large cap companies in the U.S. dramatically outperformed other equity asset classes during the quarter, extending their already substantial lead coming into the final quarter of the year. The S&P 500 was higher by 11% in the quarter, pushing its return for 2021 to 29%. From an equity style perspective, large cap growth stocks gained 12% during the quarter while value stocks gained 8%. For the year, the Russell 1000 Growth Index finished higher by 28% while the Russell 1000 Value Index was higher by nearly as much, at 25%. From a smaller company perspective, the Russell 2000 Index gained 2% during the quarter, pushing the calendar-year return to 15%. Value stocks, as measured by the Russell 2000 Value Index, significantly outperformed the Russell 2000 Growth Index for the quarter and year. For the quarter, small value stocks were higher by 4%, leaving them up 28% for the year. Growth stocks were flat for the quarter and up marginally for the year, up 3%.

Image

From a sector perspective during the quarter, gains were broad based. Several sectors produced double-digit gains, including, technology, real estate, utilities, materials, health care, consumer staples, and discretionary. Only communication services failed to post positive gains, posting 0% for the quarter overall. For the year, energy led the way with a 55% return, followed by real estate with a 46% return. Both sectors are among the smallest in the index and make up less than 6% of the S&P 500. Technology and financials were both up 35%. For context, these two sectors make up nearly 40% of the S&P 500.

Stocks outside of the U.S. trailed their U.S. counterparts during the quarter and in 2021. Developed market equity returns, as measured by the MSCI EAFE Index, gained 3% in U.S. dollar terms during the quarter. This moved the index higher by 11% for the year. The 18% return differential between EAFE and the S&P 500 was the third widest since 1997. The MSCI EAFE Index trailed the S&P 500 by 19% in 2014 and trailed by 32% in 1997 during the Asian currency crisis. In local currency terms, developed market equities outside the U.S. were up 4% in the quarter and up 19% for the year. The MSCI Emerging Markets Index was down 1% during the quarter, leaving it down 2% for the year. In local currency terms, emerging market stocks were down 1% in the quarter and flat for 2021.

Disclaimers

All market pricing and performance data from Bloomberg, unless otherwise cited. Asset class and sector performance are gross of fees unless otherwise indicated.

The opinions and analyses expressed in this newsletter are based on RMB Capital Management, LLC’s (“RMB Capital”) research and professional experience, and are expressed as of the date of our mailing of this newsletter. Certain information expressed represents an assessment at a specific point in time and is not intended to be a forecast or guarantee of future results, nor is it intended to speak to any future time periods. RMB Capital makes no warranty or representation, express or implied, nor does RMB Capital accept any liability, with respect to the information and data set forth herein, and RMB Capital specifically disclaims any duty to update any of the information and data contained in this newsletter. The information and data in this newsletter does not constitute legal, tax, accounting, investment or other professional advice. Returns are presented net of fees. An investment cannot be made directly in an index. The index data assumes reinvestment of all income and does not bear fees, taxes, or transaction costs. The investment strategy and types of securities held by the comparison index may be substantially different from the investment strategy and types of securities held by your account. The S&P 500 Index is widely regarded as the best single gauge of the U.S equity market. It includes 500 leading companies in leading industries of the U.S economy. The S&P 500 focuses on the large cap segment of the market and covers 75% of U.S. equities. The Bloomberg Barclays U.S. Aggregate Bond Index is a broad based benchmark that measures the investment grade. The Bloomberg Commodity Indices (BCOM) are a family of financial benchmarks designed to provide liquid and diversified exposure to physical commodities via futures contracts. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. Indexes are available for the U.S. and various geographic areas. Average price data for select utility, automotive fuel, and food items are also available. The Russell 1000® Growth Index measures the performance of the large- cap growth segment of the US equity universe. It includes those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values. The Russell 1000® Value Index measures the performance of the large cap value segment of the US equity universe. It includes those Russel 1000® companies with lower price-to-book ratios and lower expected growth values. The Russell 2000® Value Index measures the performance of small-cap value segment of the US equity universe. It includes those Russell 2000® companies with lower price-to-book ratios and lower forecasted growth values The Russell 2000® Growth Index measures the performance of the small-cap growth segment of the US equity.