Key Takeaways

- U.S. large-cap stocks hit over 50 new all-time highs in 2024, ending the year up 25%. U.S. small-cap stocks gained 11%, and U.S. intermediate-term bonds ended 2024 up 1%.

- Post-election, small business optimism recorded the largest month-over-month increase since July 1980. A similar shift in sentiment was noted in various CFO surveys.

- Despite sticky inflation and higher interest rates, the U.S. consumer remained resilient while U.S. government spending continued unchecked.

- The incoming administration appears focused on the challenging task of bolstering economic growth while at the same time reducing the deficit.

- The most critical element of this endeavor will be curtailing the deficit while keeping longer-term yields contained, so as not to disrupt economic expansion.

Overview

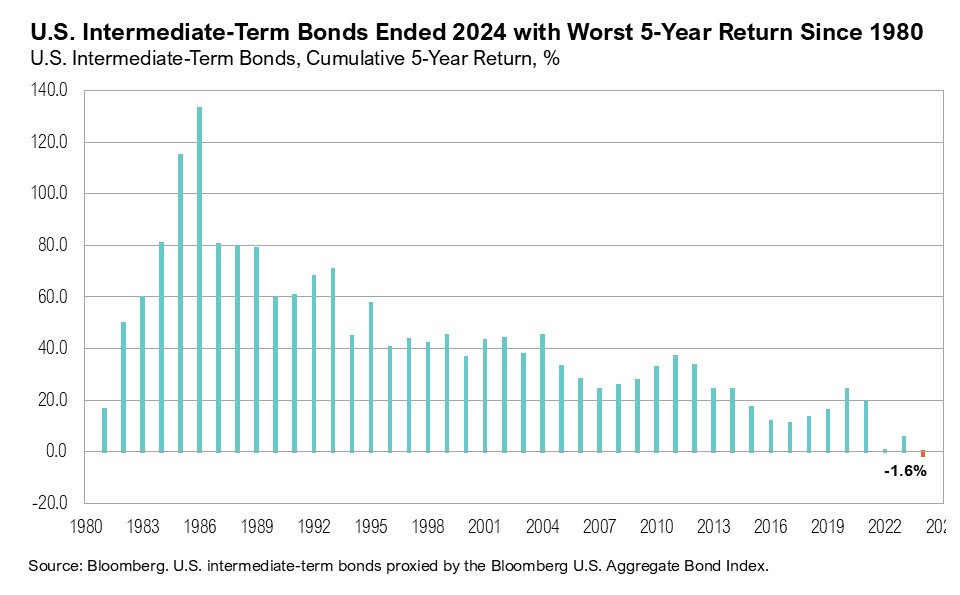

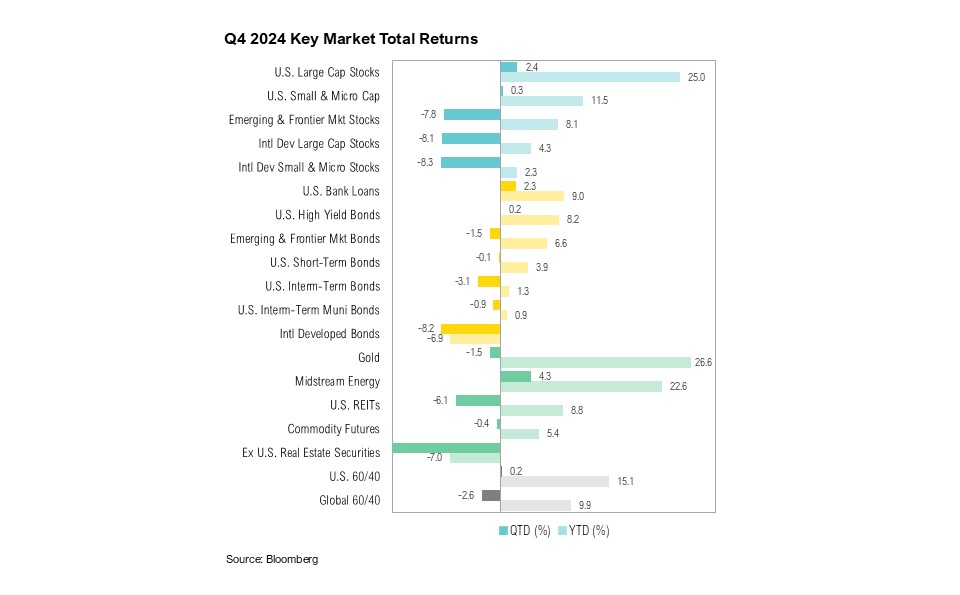

Markets ended 2024 with mixed results. U.S. large-cap stocks ended the fourth quarter up 2.4% and ended the year up 25%. The S&P 500 hit over 50 new all-time highs in 2024. Over the past two years, the S&P 500 has risen a cumulative 53% - the strongest performance since the nearly 66% increase experienced between 1997 and 1998. U.S. small-cap stocks gained 11.5% over the year after a fourth quarter gain of 0.3%. In contrast, 2024 was another challenging year for U.S. intermediate term bonds. After declining 3.1% in the fourth quarter, the Bloomberg U.S. Aggregate Bond Index ended 2024 up only 1.3%. This marks a cumulative decline of 1.6% over the past five years, making it the worst five-year return since at least 1980.

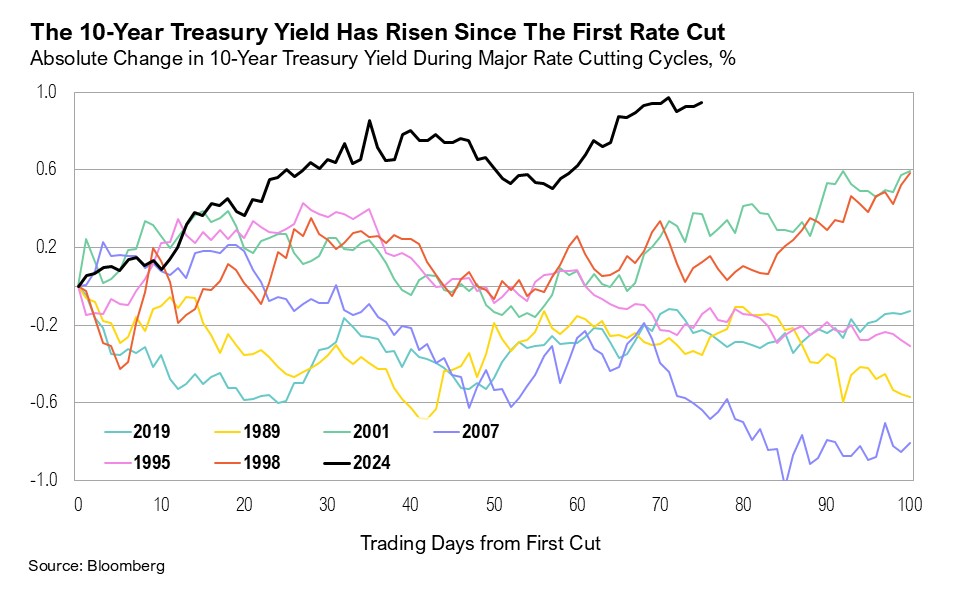

After easing to 2.4% year-over-year in September, headline inflation, as measured by the Consumer Price Index (CPI), ended the year at 2.7%, and housing inflation remained the key contributor.1 Core inflation, which excludes food and energy, ended 2024 up 3.3% and has been above 3% for 43 months.2 On September 18, with inflation still well above the official 2% target, the Federal Reserve (Fed) began to cut short-term interest rates. During the fourth quarter and across three different meetings, the Fed cut interest rates by 1.0%, bringing the year-end rate to 4.25% - 4.5%. At the December 18 Federal Open Market Committee meeting, the Fed’s economic projections indicated that committee members expected the equivalent of two 0.25% rate cuts in 2025, even though their year-end 2025 inflation expectations increased from 2.1% to 2.5%.3 The 10-year Treasury yield has climbed higher since the first rate cut in September, which is an unprecedented move relative to historical rate-cutting cycles. This pushed 30-year mortgage rates higher, to end December at 7.3%, 0.6% higher than they were prior to the first Fed interest rate cut. By early January, markets were anticipating the equivalent of only one 0.25% interest rate reduction for 2025.4

Two key factors have characterized the U.S. economy: the resilience of the U.S. consumer and the alarming rate of government deficit spending. Consumer spending continues to be robust. Online sales increased by a record $241 billion (or 9% year-over-year) over the holiday spending period.5 This is despite credit card interest rates nearing record highs at an average of 24% and the personal saving rate standing at 4.4% - well below the historical average of 8.4%. According to Mastercard Economics Chief Economist Michelle Meyer:

“The holiday shopping season revealed a consumer who is willing and able to spend but driven by a search for value as can be seen by concentrated e-commerce spending during the biggest promotional periods… Solid spending during this holiday season underscores the strength we observed from the consumer all year, supported by the healthy labor market and household wealth gains.”6

In the 2024 fiscal year, the U.S. government fiscal deficit reached $1.8 trillion, making it the largest deficit in a non-crisis or non-recessionary year on record.7 Already, the fiscal deficit for 2025 (which began in October) has surpassed $620 billion and is projected to reach $1.9 trillion by the fiscal year end.8,9 With interest rates still elevated, the interest expense on U.S. public debt rose by 20% over the past 12 months, climbing to $886 billion. This is nearly on par with national defense spending ($928 billion) and spending on health care programs ($926 billion).

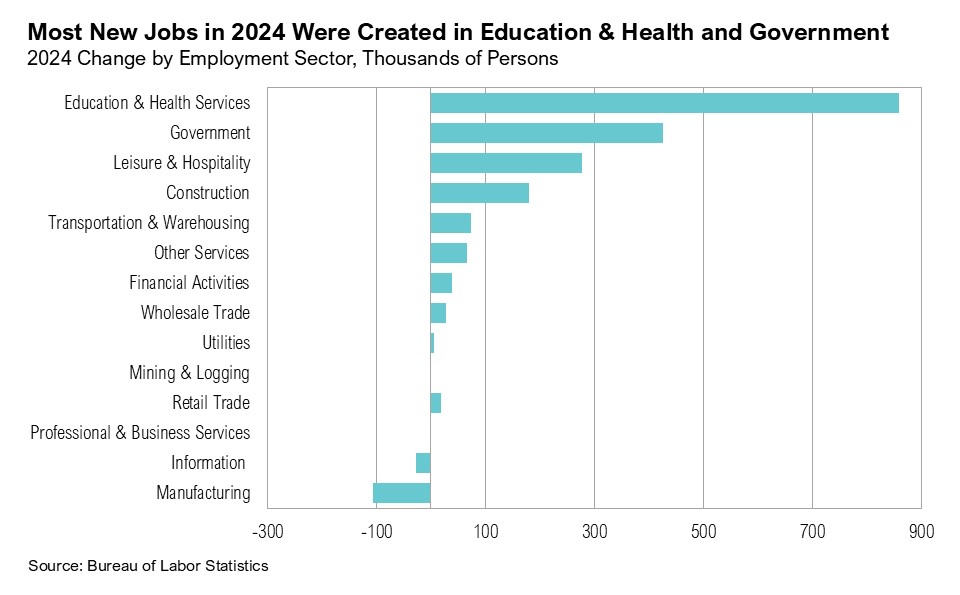

The U.S. economy expanded by an annualized 3.1% quarter-over-quarter in the third quarter, and projections for the fourth quarter are estimated to be 2.3%. The services sector remains the primary growth driver. The ISM Services PMI continued to expand throughout the fourth quarter and ended December with a reading of 54.1.10 In contrast, the manufacturing sector has contracted for eight consecutive months, and the ISM Manufacturing PMI ended 2024 with an improved reading of 49.3 - the highest reading since April. (A reading below 50 signals contraction in the sector).11 The manufacturing sector experienced the largest reduction in employment in 2024, losing over 106,000 jobs during the year, followed by the information sector, which lost over 28,000 jobs. Conversely, the education and health services sectors added nearly 860,000 jobs in 2024, and the government sector gained nearly 425,000 jobs.12 Overall, the labor market remained robust throughout 2024, and the unemployment rate finished the year near record lows at 4.1%.13

Vibes

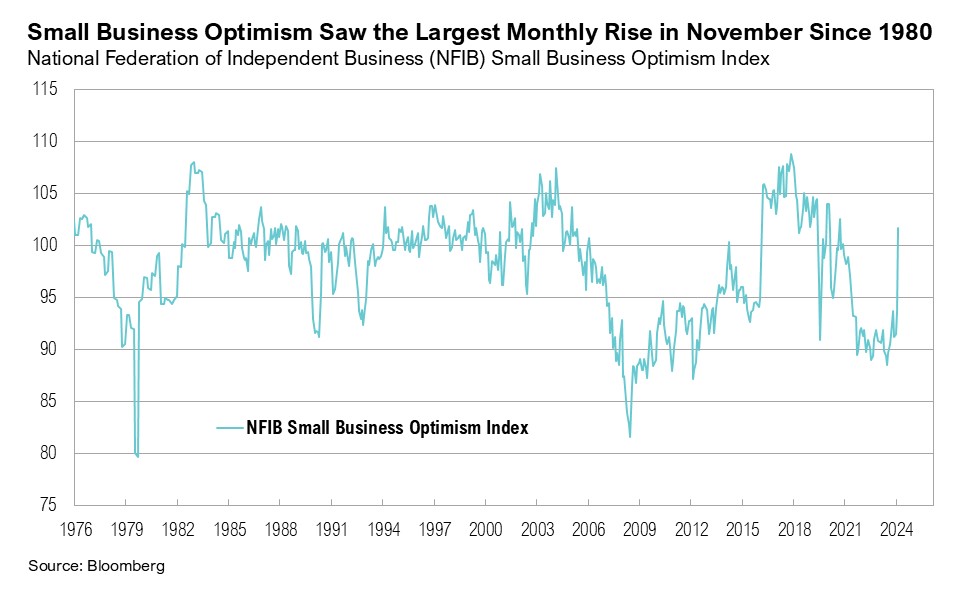

One of the defining events of 2024 was the 60th U.S. presidential election, held on November 5. After the election, which saw the Republican party emerge as the decisive winner, consumer sentiment ticked up from 72 in November to 74 in December. This was largely driven by the 16-point spike in Republican sentiment, which offset the nearly 12-point drop in Democrat sentiment. Similarly, small business optimism jumped by eight points in November - the largest month-over-month increase since July 1980.14 A similar 7.4-point spike in small business optimism was recorded in 2016. After that, the Russell 2000 Index gained 25% over the next 12 months and an annualized 13% over the next four years. The S&P 500 gained 24% over the next 12 months and an annualized 20% over the next four years.

According to the November 2024 National Federation of Independent Business (NFIB) small business survey, 36% of respondents expect the economy to improve, 18% of respondents plan to increase hiring, and 28% plan to make capital outlays.14 CFO surveys of larger companies conducted between October and November 2024 show a similar increase in optimism about the U.S. economy, and concerns about the health of the economy, company sales, and revenue declined sharply relative to the survey conducted between August and September 2024.15 Another area of markets that continued to signal economic optimism were U.S. high yield credit spreads, which ended December near historical lows, at 2.7%, and continue to suggest that the economy may achieve a “soft landing.” Further, the November Job Openings and Labor Turnover Survey (JOLTS) report, released in early January, showed signs of stability. Job openings ticked higher for the second consecutive month (the first two-month rising streak since December 2022), and the total number of job openings surpassed the 8-million mark for the first time since May 2024.16 Vibes are shifting with larger businesses too as they seek to align themselves with the new administration. Meta recently announced changes to the company’s moderation policies and practices, citing a shifting political and social landscape and a commitment to embracing free speech.17,18 The company has also announced that it will be moving its content moderation and trust and safety teams from California to Texas.17,18

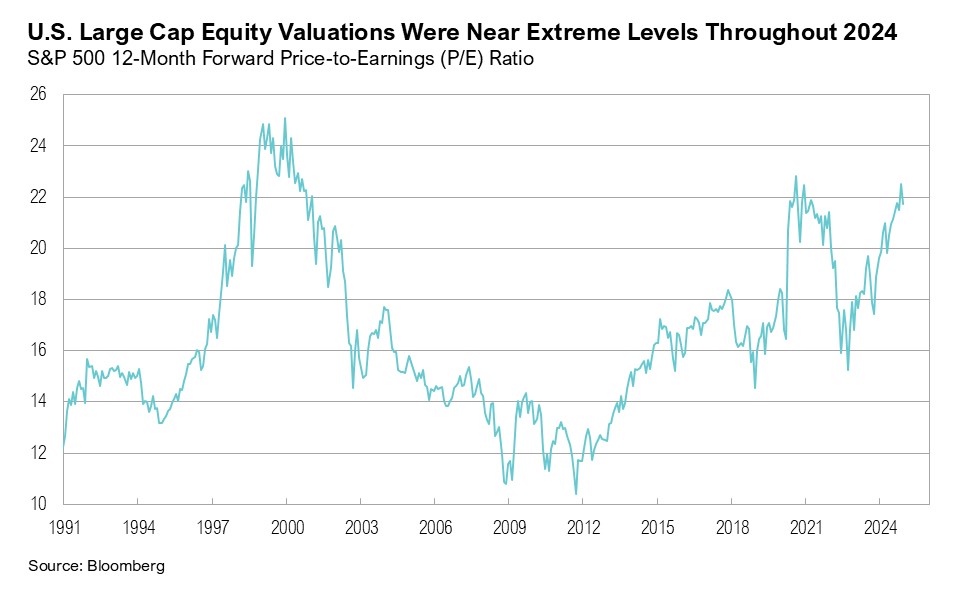

Even before post-election economic sentiment surveys showed increased optimism, equity valuations remained elevated throughout the year and even climbed back to extreme levels, akin to the tech bubble. Despite valuations at extremes, U.S. large-cap returns were once again above average. With only 19% of S&P 500 constituents outperforming the broader index over the past year, returns remain substantially driven by a handful of mega-cap technology stocks, including Nvidia (up 171% in 2024), Meta (up 65%), Tesla (up 63%), and Amazon (up 44%). The Magnificent Seven now account for over a third of the S&P 500, up from a fifth of the index in 2022. Earnings growth for the S&P 500 is expected to be 15% for 2025.19 In contrast, earnings growth for the Russell 2000 index is expected to accelerate by 40% in 2025.20

With the new administration taking office on January 20, President-Elect Donald Trump has already announced several key nominations for Cabinet posts and White House roles. Among these is Scott Bessent (a former Democrat donor), who has been nominated as Treasury Secretary.21,22 Bessent has outlined a “3-3-3” target, which includes achieving 3% economic growth, reducing the federal deficit to 3% of GDP by 2028, and increasing daily energy production by the equivalent of 3 million barrels of oil—approximately a 20% increase from current levels.23,24,25 When asked about his decision to accept the nomination, Bessent remarked:

“This election cycle is the last chance for the U.S. to grow our way out of this mountain of debt…”26

Bessent’s remark shows a stark contrast between the incoming and outgoing administrations’ perspectives on the U.S. fiscal deficit burden and a shift in attitude about approaching the issue. At a Wall Street Journal CEO Summit, held on December 10, current Treasury Secretary Janet Yellen remarked:

“Well, I am concerned about fiscal sustainability, and I am sorry that we haven’t made more progress. I believe that the deficit needs to be brought down, especially now that we’re in an environment of higher interest rates.”27

Conquering the rocky mountain size of the fiscal deficit is daunting; however, there is reason for optimism. In addition to Bessent, Trump has also announced the creation of the Department of Government Efficiency (DOGE). Led by Elon Musk and Vivek Ramaswamy, the department will seek to improve government accountability and efficiency within federal agencies.28 While DOGE will not be an official government department but rather an advisory board, it could result in lightening the U.S. fiscal deficit burden.

The new administration is expected to usher in a more supportive regulatory environment for digital assets. Bitcoin surged 43% in the fourth quarter and ended 2024 up 130%. In a noteworthy move, Trump has appointed David Sacks as the nation’s first Crypto and Artificial Intelligence (AI) Czar. In this advisory role, Sacks will facilitate communication between government officials and tech industry leaders while working to establish a regulatory framework that supports the growth of digital currencies.29

Markets

U.S. equity markets fared significantly better than their international counterparts over the fourth quarter. U.S. large-cap stocks gained 2.4% while international developed large-cap stocks ended the quarter down 8.1%. Similarly, while U.S. small-cap stocks ended the quarter flat after gaining only 0.3%, international developed small-cap stocks dropped 8.3% over the quarter. Emerging and frontier market stocks ended the fourth quarter down 7.8%. The U.S. dollar ended the month at its highest level since November 2022. Fixed income markets exhibited similar dynamics: while U.S. intermediate-term bonds ended the fourth quarter down 3.1%, international developed market bonds ended the quarter down 8.2%.

Despite ending the fourth quarter down 1.5%, gold ended 2024 up 26.6%, setting over 30 new record highs. After reaching a one-year low of $65.8 per barrel on September 10, West Texas Intermediate (WTI) crude oil ended the year at $71.7 per barrel. Despite rising oil prices, U.S. national average gasoline prices reached a three-year low of $3.02 on December 12.30

Looking Forward

The incoming administration appears focused on bolstering economic growth, while at the same time reducing the deficit. The most critical element of this endeavor will be curtailing the deficit and, in the process, keeping longer-term yields contained to not disrupt the economic expansion.

While the Federal Reserve can dictate short-term interest rates through policy decisions, they have less control over longer-term rates. Since the first rate cut in September, longer-term yields have reacted with a unique vibe, moving higher than other rate-cutting cycles. That’s not to say a rise in bond yields is bad, per se, but unless it is driven by higher long-term growth prospects that translate to higher corporate earnings, rather than fiscal irresponsibility or other perceived policy errors, it could negatively impact risky asset valuations. It will now be up to fiscal policymakers to thread this needle. If they can, it will allow the continuation of government policies that support economic growth, which are critical for supporting equity and credit markets.

Our position on the markets remains unchanged. We continue to be cautious with risk assets as the current cycle plays out. With the US election behind them, market participants have more clarity on the direction of U.S. policy. Most importantly, the newly appointed administration seems to bring a renewed focus on the deficit and better alignment with the Fed’s policy of trying to grow the U.S. out of massive deficits. We expect the yield curve to continue to normalize and inflation appears to be contained, but risk to the upside has increased.

We expect the increased volatility in markets to continue in the coming weeks and months. Although lower asset prices would be a welcome development and an opportunity to put additional capital to work, equity valuations suggest that there is no rush. Stock returns and corporate earnings have been very concentrated and equity valuation continues to be above average, even when excluding the top performing stocks. We remain biased towards high-quality companies within our core stock portfolios. We have been well-positioned within core bond portfolios with a low weight toward shorter-duration corporate bonds and a higher weight toward longer-duration treasury bonds. We believe clients are best served reminding themselves of the timeless principles of patience and diversification. The key to successful investing is often remaining committed to long-term investment plans.

Citations

- BLS: https://www.bls.gov/news.release/cpi.nr0.htm

- FRED: https://fred.stlouisfed.org/series/CPILFESL#0

- Federal Reserve: https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20241218.pdf

- CME FedWatch: https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

- Adobe Analytics: https://news.adobe.com/news/2025/1/newsroom-article-text-marquee

- Mastercard: https://newsroom.mastercard.com/news/press/2024/december/mastercard-spendingpulse-total-u-s-retail-sales-grew-3-8-this-holiday-season-online-remained-choice-for-consumers-increasing-6-7-yoy/

- Bipartisan Policy Center: https://bipartisanpolicy.org/report/deficit-tracker/

- U.S. Department of Treasury: https://www.fiscal.treasury.gov/files/reports-statements/mts/mts1124.pdf

- Congressional Budget Office: https://www.cbo.gov/system/files/2024-06/60039-By-the-Numbers.pdf

- ISM: https://www.ismworld.org/supply-management-news-and-reports/reports/ism-report-on-business/services/december/

- ISM: https://www.ismworld.org/supply-management-news-and-reports/reports/ism-report-on-business/pmi/december/

- BLS: https://www.bls.gov/news.release/empsit.nr0.htm

- BLS: https://www.bls.gov/news.release/empsit.t17.htm

- NFIB: https://www.nfib.com/wp-content/uploads/2024/12/SBET-November-2024.pdf

- Federal Reserve Bank of Richmond: https://www.richmondfed.org/research/national_economy/cfo_survey/data_and_results/2024/20241204_data_and_results

- BLS: https://www.bls.gov/jlt/

- NBC News: https://www.nbcnews.com/tech/social-media/meta-ends-fact-checking-program-community-notes-x-rcna186468

- AP News: https://apnews.com/article/meta-facts-trump-musk-community-notes-413b8495939a058ff2d25fd23f2e0f43

- FactSet: https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_010325.pdf

- Franklin Templeton: https://www.franklintempleton.lu/articles/2024/royce-investment-partners/the-prospects-for-extended-us-small-cap-outperformance

- NY Times: https://www.nytimes.com/2024/11/23/us/politics/scott-bessent-treasury-profile.html

- Wall Street Journal: https://www.wsj.com/politics/elections/the-ex-soros-executive-who-is-trumps-new-obsession-4be2d493

- CNBC: https://www.cnbc.com/2024/11/25/scott-bessent-what-trumps-treasury-pick-could-mean-for-markets.html

- Wall Street Journal: https://www.wsj.com/politics/policy/scott-bessent-sees-a-coming-global-economic-reordering-he-wants-to-be-part-of-it-533d6e71

- EIA: https://www.eia.gov/dnav/pet/hist/leafhandler.ashx?n=pet&s=mcrfpus2&f=m

- AP News: https://apnews.com/article/treasury-trump-biden-finance-elections-bessent-transition-8df8be88e4c83df4b9f3c4238966e79d

- The Hill: https://thehill.com/business/budget/5035194-yellen-budget-deficit-biden-administration/

- CNN: https://edition.cnn.com/2024/11/12/politics/elon-musk-vivek-ramaswamy-department-of-government-efficiency-trump/index.html

- Reuters: https://www.reuters.com/world/us/trump-appoints-former-paypal-coo-david-sacks-ai-crypto-czar-2024-12-06/

- AAA: https://gasprices.aaa.com/

Index Definitions

The S&P 500 Index is widely regarded as the best single gauge of the United States equity market. It includes 500 leading companies in leading industries of the U.S. economy. The S&P 500 focuses on the large cap segment of the market and covers approximately 75% of U.S. equities.

The Bloomberg Barclays U.S. Aggregate Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. Duration is roughly 5 years.

The Bloomberg U.S. Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

The Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected and historical growth rates.

The Russell 1000® Growth Index measures the performance of the large- cap growth segment of the US equity universe. It includes those Russell 1000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years).

The Russell 2000® Index measures the performance of the small-cap segment of the US equity universe. It includes approximately 2000 of the smallest US equity securities in the Russell 3000 Index based on a combination of market capitalization and current index membership. The Russell 2000 Index represents approximately 10% of the total market capitalization of the Russell 3000 Index. Because the Russell 2000 serves as a proxy for lower quality, small cap stocks, it provides an appropriate benchmark for RMB Special Situations.

MSCI EAFE Index*: an equity index which captures large and mid-cap representation across 21 of 23 Developed Markets countries around the world, excluding the U.S. and Canada. With 926 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Emerging Markets Index* measures equity market performance in the global emerging markets universe. It covers over 2,700 securities in 21 markets that are currently classified as EM countries. The MSCI EM Index universe spans large, mid and small cap securities and can be segmented across all styles and sectors.

The U.S. Dollar Index is used to measure the value of the dollar against a basket of six foreign currencies: the euro, Swiss franc, Japanese yen, Canadian dollar, British pound, and Swedish krona.

The Deutsche Bank EM FX Equally Weighted Spot Index, an equal-weighted basket of 21 emerging market currencies.

MSCI U.S. REIT Index is a free float-adjusted market capitalization weighted index that is comprised of equity Real Estate Investment Trusts (REITs). The index is based on the MSCI USA Investable Market Index (IMI), its parent index, which captures the large, mid and small cap segments of the USA market. With 150 constituents, it represents about 99% of the US REIT universe and securities are classified under the Equity REITs Industry (under the Real Estate Sector) according to the Global Industry Classification Standard (GICS®), have core real estate exposure (i.e., only selected Specialized REITs are eligible) and carry REIT tax status.

MSCI China NR Index: designed to measure the performance of the large and mid cap segments of the Chilean market. With 12 constituents, the index covers approximately 85% of the Chile equity universe.

MSCI South Africa NR Index: designed to measure the performance of the large and mid cap segments of the South African market. With 37 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in South Africa.

*Source: MSCI.MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Performance Disclosures

All market pricing and performance data from Bloomberg, unless otherwise cited. Asset class and sector performance are gross of fees unless otherwise indicated.

The opinions and analyses expressed in this newsletter are based on Curi RMB Capital, LLC’s (“Curi RMB Capital”) research and professional experience are expressed as of the date of our mailing of this newsletter. Certain information expressed represents an assessment at a specific point in time and is not intended to be a forecast or guarantee of future results, nor is it intended to speak to any future time periods. Curi RMB Capital makes no warranty or representation, express or implied, nor does Curi RMB Capital accept any liability, with respect to the information and data set forth herein, and Curi RMB Capital specifically disclaims any duty to update any of the information and data contained in this newsletter. The information and data in this newsletter does not constitute legal, tax, accounting, investment or other professional advice. Returns are presented net of fees. An investment cannot be made directly in an index. The index data assumes reinvestment of all income and does not bear fees, taxes, or transaction costs. The investment strategy and types of securities held by the comparison index may be substantially different from the investment strategy and types of securities held by your account. RMB Asset Management is a division of Curi RMB Capital.