Markets

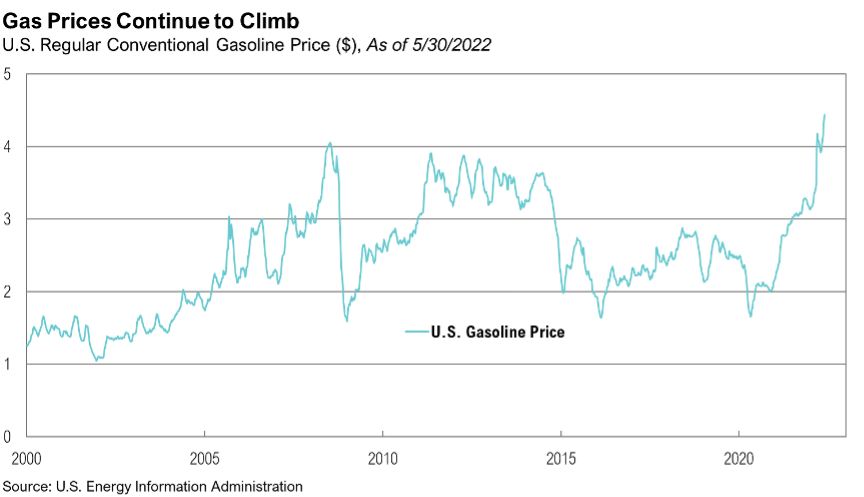

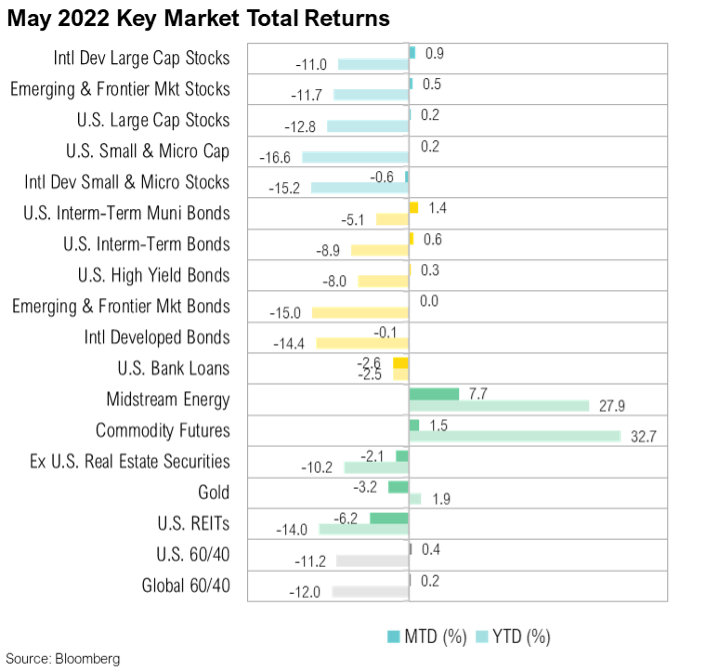

On the surface, May might seem like a reprieve from 2022’s notorious volatility as the S&P 500 index slightly increased by 0.2%. However, intra-month returns tell a more dramatic story. On May 20, the index was down over 5% for the month to date before rallying over the last week-and-a-half to recover its losses. From a style perspective, value stocks (+1.9%), as measured by the Russell 1000 Value Index, outperformed growth stocks (-1.9%), as measured by the Russell 1000 Growth Index. Energy stocks, which represent 8.4% of the value index compared to just 0.6% in the growth index,1,2 were a major contributor to value’s relative performance, finishing the month as the top-performing sector, up 16%. The price of West Texas Intermediate (WTI) crude oil is now $115 per barrel, its highest level since March. Despite higher prices, oil producers remain hesitant to ramp up supply. Rig counts are still 16% lower than in February 2020 when crude was trading around $60 per barrel.3 U.S. crude oil inventories excluding the U.S. Special Petroleum Reserve are at just 414 million barrels per week, down from 480 million a year ago.4 With the U.S. banning imports of Russian oil and natural gas back in March5 and OPEC unwilling to meaningfully increase production this year so far,6 U.S. producers will likely need to significantly ramp up production to curb further price increases. Year-to-date, the average U.S. regular conventional gas price is up 41% and currently sits at $4.40 a gallon, surpassing the previous high set back in July 2008 at $4.05 a gallon.7

In May, stocks outside of the U.S. outperformed their U.S. counterparts. Foreign developed and emerging market equity returns, as measured by the MSCI EAFE and Emerging Market Indexes, rose 0.9% and 0.5% in U.S. dollar terms. A contributing factor was the weakening of the U.S. dollar over the month as the U.S. Dollar Index fell 1.2%. U.S. REITs were the worst-performing asset class in May, falling 6.2%, as 30-year fixed mortgage rates remained above 5%. Rising interest rates can serve to cool real estate markets since they reduce mortgage affordability and–eventually–property values.

Within fixed income, the Bloomberg U.S. Aggregate Bond Index rose 0.6%, ending its streak of five straight months of negative returns. The 10-year Treasury yield hit 3% in May for the first time since December 2018, which coincidentally was the end of the last Federal Reserve hiking cycle. High-yield bonds slightly lagged behind higher quality bonds, rising just 0.3%. Finally, bank loans were the worst performing fixed income asset class, returning -2.6%. U.S. loan funds posted their largest weekly outflow since the onset of the pandemic, losing $1.56 billion for the week ended May 18, as investors started to worry about deteriorating loan fundamentals.8

Economic Scenarios

The Federal Reserve is charged with an excruciatingly difficult task – slow down the economy to cool inflation. Federal Reserve Chairman Jerome Powell hinted at this fragile dynamic in a recent interview in May with the Wall Street Journal:

“It’s challenging because unemployment is very low already and because inflation is very high. But I will just say there are pathways for us to be able to moderate demand, get demand and supply back in alignment, and get inflation back down while also having a strong labor market. Doesn’t mean that the unemployment rate needs to remain 3.6%, which is a very, very low rate…You’d still have quite a strong labor market if unemployment were to move up a few ticks.”9

In stark contrast to its accommodative policy stance for most of the past fourteen years, the Fed wants to slow demand to cool off inflation and is willing to sacrifice today’s low unemployment rate to do it. Based on what the Fed does and how the economy responds, three scenarios seem possible – (1) a soft landing (Goldilocks), (2) a recession brought on by policy tightening, or (3) stagflation. The first scenario would be more constructive (bullish) for risky assets, whereas the last two scenarios would be more challenging–or bearish–at least in the short term.

Goldilocks

The ideal outcome for markets is a soft landing or what we call the “Goldilocks” outcome. In this scenario, the Federal Reserve’s monetary tightening slows the economy just enough to cool inflation, but it avoids a recession, ultimately prolonging the current economic recovery. This scenario would be generally good for asset prices and probably resume stocks’ bull market trajectory.

Despite a steady stream of negative headlines, this possibility should not be dismissed. Many of the factors contributing to the Fed’s inflation headache – supply chain disruptions, China’s zero-COVID policy and resulting lockdowns, and the Russian/Ukraine conflict – could provide significant pain relief if they shift. Of course, these events are out of the Fed’s control, but if any are resolved, it would ease inflation and reduce the amount of policy tightening needed. With such a strong labor market, the Fed may have some cover to reduce demand without tipping the economy into recession. The unemployment rate sits at 3.6%, which other than pre-pandemic, was last experienced during the 1970s.10 Further, there are 11.4 million job openings.11

Recession

In this scenario, aggressive tightening by the Fed could push the economy into recession sooner than expected, and the resulting decline in demand could change the broader economic outlook. While painful in the short term, the recession could set the stage for a more healthy and sustainable recovery than the stimulus-driven bounce experienced after the pandemic.

Working against the Fed is the need to unwind the unprecedented monetary stimulus provided over the past fourteen years, including holding interest rates at 0% for many years and amassing a balance sheet that once held nearly $9 trillion worth of bonds.12 This level of stimulus served as enormous tailwinds for asset prices, and reversing these policies will have the opposite effect. Last week, the Fed raised short term interest rates by 75 basis points, bringing the total for this tightening cycle to 150 basis points. The Fed is expected to hike another 50 - 75 basis points at the next FOMC meetings in July. In addition, the Fed intends to decrease its balance sheet holdings by $47.5 billion per month starting in June, eventually increasing the amount to $95 billion per month in September.13

Although the National Bureau of Economic Research (NBER) officially decides when a recession has begun, informally, a recession is characterized by two consecutive quarters of negative real GDP growth.14 In the first quarter, the U.S. economy produced annualized GDP growth of -1.5%, meaning that if the second quarter is also negative, it could imply a recession – the second in just over two years. Regardless of labels, the U.S. economy is clearly slowing. In the current economic recovery starting in July 2020, real GDP growth has averaged an annualized 9.3%, including a robust 5.5% in 2021.15 GDP is made up of four components—consumption, investment, government spending, and net trade—of which consumption carries the most weight.15 In the U.S. Bureau of Economic Analysis’ first quarter 2021 report, consumption grew at an impressive 3.1%, investment was essentially flat at 0.5%, government spending fell 2.7%, and net trade was -23.7%. The -23.7% net trade contraction contributed -3.23% to the headline real GDP number, dragging down respectable consumption growth. Some economists believe the extreme net trade number is a false signal for things to come. According to Ian Shepherdson, Chief Economist at Pantheon Macroeconomics:

“This is noise, not signal. The economy is not falling into recession. Net trade has been hammered by a surge in imports, especially of consumer goods, as wholesalers and retailers have sought to rebuild inventory. This cannot persist much longer, and imports in due course will drop outright, and net trade will boost GDP growth in Q2 and/or Q3.”16

The Atlanta Fed’s GDPNow, which provides a forecast of the official GDP estimate before its release, currently projects second-quarter real GDP growth at an annualized 0.9%, fueled by strong consumption growth of 2.5%.17 Given consumption makes up roughly two-thirds of GDP and is seemingly its strongest component, it also poses the biggest risk to economic strength.

Stagflation

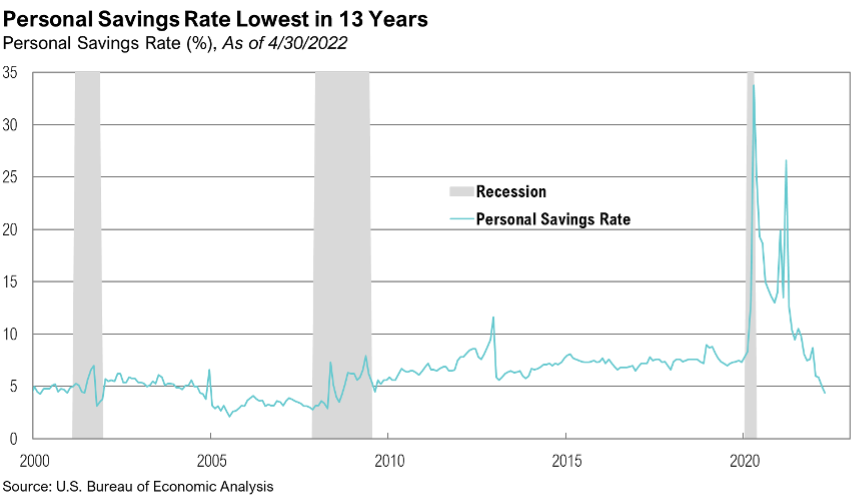

Inflation has outpaced wage growth for over a year now, and the most recent U.S. real wage growth rate, released at the end of April, was -3.7% on a year-over-year basis.18 This is no doubt causing some stress to once-strong consumer balance sheets, and cracks are starting to show. Revolving consumer credit is back up near all-time highs again after collapsing 12% in February 2020 due to pandemic stimulus.19 At the end of April, the personal savings rate fell to 4.4%, its lowest level since August 2008, a period when the economy was in a recession.20 While the U.S. consumer should not be underestimated, if inflation continues at its current blistering pace, consumers will not be able to sustain enough spending to drive any meaningful economic growth.

Stagflation is defined by slow economic growth and relatively high unemployment—or economic stagnation—and accompanied by rising prices (i.e., inflation).21 An important component of stagflation is the unemployment rate. Typically, the unemployment rate is inversely related to inflation. When the economy is expanding rapidly, prices rise, and the unemployment rate falls. In a stagflation regime, the opposite happens, usually when the money supply is expanding while supply is being constrained by some exogenous shock. The 1970s and early 1980s are textbook examples of this phenomenon. During these two decades, inflation averaged 6.3%, real Gross Domestic Product (“GDP”) growth averaged 3.2% per year, and the unemployment rate averaged 6.7%. In this case, the exogenous shock was the 1973 Organization of the Petroleum Exporting Countries (OPEC) oil embargo against western nations during the Arab-Israeli war. OPEC restricted supply in retaliation for the U.S. decision to re-supply the Israeli military and to gain leverage in post-war peace negotiations.22 This caused upward pressure on oil prices, and oil rose from $25/barrel in 1972 to a peak of $140/barrel in 1980.23 Today has some striking parallels. Oil futures traded in negative territory in April 2020 as a result of COVID-19 lockdowns. Over the next two years, the price of a barrel of WTI crude oil rose to over $115 per barrel, exacerbated by a new wartime embargo, this time imposed by Western nations to restrict the demand for Russian oil in retaliation for the Russian invasion of Ukraine.24

If stagflation is more specifically defined as periods with inflation above 5%, real GDP growth less than 2% per year, and unemployment above 6%, there have been 41 months (less than 5% of the time) since 1947 that have fit these criteria. Most of these months (85%) happened from 1973 to 1982, and 68% occurred when the economy was in recession. Today, inflation is at 8.2%, and first-quarter 2022 real GDP growth was -1.5% (annualized), both well within the defined boundaries of stagflation. While the May unemployment rate was still low at 3.6%, this measure usually lags behind current economic conditions. An earnings slowdown could result in hiring freezes and layoffs and subsequently slow down a currently red-hot U.S. labor market relatively quickly.

Looking Forward

The future is uncertain, and the three scenarios presented may not be mutually exclusive. Regardless of the unknowns, we do believe that incoming inflation data and the Fed’s response over the next few months remain crucial to determining where the economy—and markets—are headed.

At RMB, our goal is to position our client’s portfolios to be able to withstand and thrive in more than one economic outcome. We believe there will be continued volatility in both equity and fixed income markets as the Federal Reserve continues with their plan to increase interest rates in the face of raising inflation. Markets continue to price in additional interest rate hikes through the rest of 2022. With headline inflation currently at 8.6% annualized and continuing to surprise on the upside, the Fed’s ability to engineer a “soft landing” of taming inflation without hindering growth is at the forefront of investor’s minds.

At RMB, we feel that strong fundamentals and continuation of the economic recovery that started late last year should help markets over the longer term but the risks in the short-term are continuing to rise. Stock valuations have come back to average levels as thus far earnings have held up better than prices in 2022. While earnings growth remains positive, we are starting to see signs of that growth slowing down as companies are grappling with continued headwinds such as high inflation, supply chain disruptions, labor shortages and the ongoing conflict in Europe. We continue to believe that the income component of our client’s investment portfolios – the interest paid from owning bonds and stock dividends – will be a more important factor of investment returns going forward. To help weather the short-term volatility we are likely to experience in the coming months, we continue to recommend clients stick to their long-term investment allocation targets and use the market volatility to their benefit by taking advantage of rebalancing opportunities to selectively make changes within portfolios. During volatile times, the key to successful investing is often remaining calm and committed to long-term investment plans. We remain optimistic that the strategies we have in place for our clients will drive long term success despite the volatility we are currently experiencing.

1. Blackrock: https://www.ishares.com/us/products/239708/ishares-russell-1000-value-etf

2. Blackrock: https://www.ishares.com/us/products/239706/ishares-russell-1000-growth-etf

3. Baker Hughes: https://rigcount.bakerhughes.com/na-rig-count

4. EIA: https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=WCESTUS1&f=W

5. WSJ: https://www.wsj.com/articles/russian-oil-producers-stay-one-step-ahead-of-sanctions-11654076614

7. EIA: https://www.eia.gov/petroleum/gasdiesel/

10. U.S. Bureau of Labor Statistics: https://fred.stlouisfed.org/series/UNRATE

11. CNBC: https://www.cnbc.com/2022/06/01/the-job-market-is-still-hot-for-now.html

12. Federal Reserve: https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm

13. Federal Reserve: https://www.federalreserve.gov/newsevents/pressreleases/monetary20220504b.htm

14. Investopedia: https://www.investopedia.com/terms/r/recession.asp

15. BEA: https://www.bea.gov/sites/default/files/2022-05/gdp1q22_2nd.pdf

16. CNBC: https://www.cnbc.com/2022/04/28/us-q1-gdp-growth.html

17. Federal Reserve Bank of Atlanta: https://www.atlantafed.org/cqer/research/gdpnow?panel=3

18. U.S. Bureau of Labor Statistics: https://fred.stlouisfed.org/series/LES1252881600Q#0

19. Federal Reserve: https://www.federalreserve.gov/releases/g19/current/

20. Bureau of Economic Analysis: https://www.bea.gov/data/income-saving/personal-saving-rate

21. Investopedia: https://www.investopedia.com/terms/s/stagflation.asp#citation-10

22. Office of the Historian: https://history.state.gov/milestones/1969-1976/oil-embargo

23. Macro Trends: https://www.macrotrends.net/1369/crude-oil-price-history-chart

24. WSJ: https://www.wsj.com/articles/u-s-planning-to-ban-russian-oil-imports-11646746787?mod=article_inline

All market pricing and performance data from Bloomberg, unless otherwise cited. Asset class and sector performance are gross of fees unless otherwise indicated.

Index Definitions

Bloomberg Barclays U.S. Aggregate: The Bloomberg Barclays Capital U.S. Aggregate Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. Duration is roughly 5 years. The index is roughly 35% US Treasuries, 32% MBS / CMBS, 20% Corporate bonds, 6% Government related and 7% other types of bonds. There are no TIPS in this index.

S&P 500 Index: The S&P 500 is widely regarded as the best single gauge of the United States equity market. It includes 500 leading companies in leading industries of the US economy. The S&P 500 focuses on the large-cap segment of the market and covers approximately 75% of U.S. equities.

MSCI EAFE Index* is an equity index which captures large and mid-cap representation across 21 of 23 Developed Markets countries around the world, excluding the U.S. and Canada. With 926 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI ACWI Index*, MSCI’s flagship global equity index, is designed to represent performance of the full opportunity set of large- and mid-cap stocks across 23 developed and 26 emerging markets. It covers more than 3,000 constituents across 11 sectors and approximately 85% of the free float-adjusted market capitalization in each market.

The MSCI EAFE Small Cap Index* is an equity index which captures small cap representation across Developed Markets countries around the world, excluding the U.S. and Canada. With 2,323 constituents, the index covers approximately 14% of the free float adjusted market capitalization in each country.

The MSCI Europe Index* represents the performance of large and mid-cap equities across 15 developed countries in Europe. It covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Emerging Markets Index* measures equity market performance in the global emerging markets universe. It covers over 2,700 securities in 21 markets that are currently classified as EM countries. The MSCI EM Index universe spans large, mid and small cap securities and can be segmented across all styles and sectors.

The MSCI Japan Index* is designed to measure the performance of the large and mid cap segments of the Japanese market. With 321 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in Japan.

The Russell 1000 Index is a stock market index that tracks the highest-ranking 1,000 stocks in the Russell 3000 Index, which represent about 93% of the total market capitalization of that index.

The Russell 1000 Index is a stock market index that tracks the highest-ranking 1,000 stocks in the Russell 3000 Index, which represent about 93% of the total market capitalization of that index.

The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected and historical growth rates.

The Russell 1000 Growth Index measures the performance of the large- cap growth segment of the US equity universe. It includes those Russell 1000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years).

The Russell 2000 Index is a subset of the Russell 3000 Index, representing about 8% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership.

The Russell 2000 Value Index measures the performance of the large- cap value segment of the US equity universe. It includes those Russell 2000 companies with relatively lower price-to-book ratios, lower I/B/E/S. forecast medium term (2 year) growth and lower sales per share historical.

The Russell 2000 Growth Index measures the performance of the large- cap growth segment of the US equity universe. It includes those Russell 2000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years).

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

The opinions and analyses expressed in this newsletter are based on RMB Capital Management, LLC’s (“RMB Capital”) research and professional experience are expressed as of the date of our mailing of this newsletter. Certain information expressed represents an assessment at a specific point in time and is not intended to be a forecast or guarantee of future results, nor is it intended to speak to any future time periods. RMB Capital makes no warranty or representation, express or implied, nor does RMB Capital accept any liability, with respect to the information and data set forth herein, and RMB Capital specifically disclaims any duty to update any of the information and data contained in this newsletter. The information and data in this newsletter does not constitute legal, tax, accounting, investment or other professional advice. Returns are presented net of fees.

An investment cannot be made directly in an index. The index data assumes reinvestment of all income and does not bear fees, taxes, or transaction costs. The investment strategy and types of securities held by the comparison index may be substantially different from the investment strategy and types of securities held by your account.

*Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.