Body

The Consumer

Global markets have been roiled by a succession of blows this year – higher bond yields, lingering post-pandemic supply chain imbalances, a commodity price shock exaggerated by the war in Ukraine, and lockdowns across most major cities in China. Although none of these are trivial, markets have been able to brush off similarly worrying events in recent years because policymakers, particularly the Federal Reserve, have been quick to step in with support, typically in the form of lower interest rates, quantitative easing, or both. But markets currently have a new threat, one that has not been experienced in several decades – stubbornly high inflation.

Not only is inflation high, but it is jarringly so. As such, it is front-and-center for consumers and policymakers alike, and the fear of it has surpassed worries of an economic slowdown. In April, the University of Michigan Index of Consumer Sentiment hit 65.2, one of its lowest readings in four decades. From the accompanying press release:

“The downward slide in confidence represents the impact of uncertainty, which began with the pandemic and was reinforced by cross-currents, including the negative impact of inflation and higher interest rates.”1

Similarly, the policy response to inflation was crystallized by comments from Federal Reserve Chairman Jerome Powell after the well-telegraphed 0.5% rate hike in early May, the first hike of that magnitude in 22 years:

“Inflation is much too high and we understand the hardship it’s causing, and we're moving expeditiously to bring it back down. Against this backdrop, today the FOMC raised its policy interest rate by 1/2 percentage point and anticipates that ongoing increases in the target rate for the federal funds rate will be appropriate.”2

It is this fear – of the hardship inflation and tighter monetary policy could cause – that has driven market returns in recent weeks. In addition to eroding purchasing power and investment returns, inflation also undermines the current value of financial assets, including stocks and bonds. This dynamic can become self-reinforcing if elevated inflation persists and consumers lose the incentive to defer much-needed current income for the prospects of potential future gains. At the end of April, year-over-year inflation was 8.3%, a slight dip from the prior month’s 8.5%, whereas a U.S. balanced portfolio of 60% stocks and 40% bonds yielded just 2.1%.3 Either inflation must come down, or the value of many assets may need to decline to levels that justify holding them for the long term.

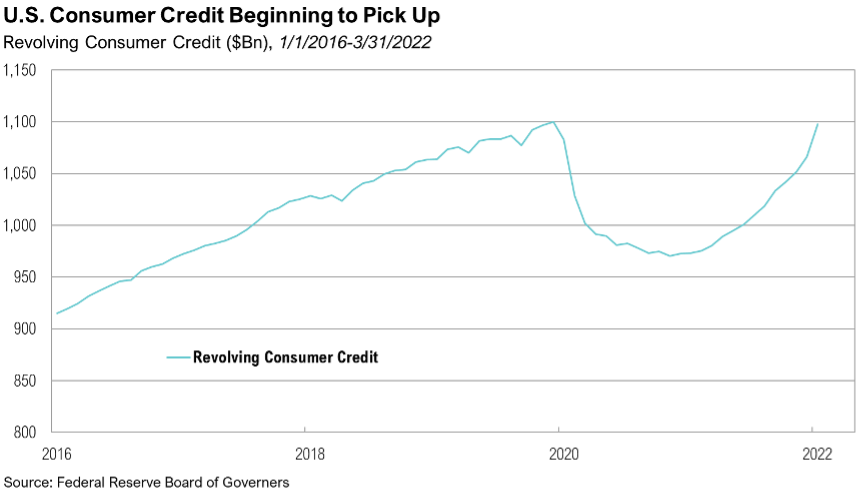

Persistent inflation can also prevent consumers from investing, especially when it exceeds wage growth. Over the past 12 months, wage growth has been 4.6% – a full 3.7% lower than inflation.4,5 The inability of wages to keep pace with inflation is showing up in revolving credit balances, which jumped 12.8% in March on a year-over-year basis, the largest increase since April 2001.6 While the absolute levels of consumer credit are not yet concerning, the rapid rate of change speaks to U.S. consumers’ precarious situation. The personal savings rate over the past year tells a similar story. In March 2022, it hit 6.2%, substantially lower than the stimulus-fueled 26.6% logged in March 2021 and a material deterioration from the December 2021 reading of 8.4%. The current reading is the lowest savings rate since December 2013.7

Image

Corporate Earnings

April was an important month in the earnings calendar, as nine of the top ten largest U.S. companies reported first-quarter results, including all five “FAANG” stocks: Meta (formerly Facebook), Apple, Amazon, Netflix, and Alphabet (formerly Google). The S&P 500, a proxy for the overall U.S. stock market, is on track to report first-quarter earnings growth of 7.1% (on a year-over-year basis).8 This represents the first quarter of single-digit earnings growth since the fourth quarter of 2020. Digging a little deeper, 80% of companies in the S&P 500 are beating earnings per share estimates, slightly above the five-year average of 77%.8 However, companies are reporting earnings just 3.4% above estimates, which is well below the five-year average of 8.9%. While on the surface these numbers appear respectable, the S&P 500 is trading at 17.6 times forward earnings, which is still above the 10-year average of 16.9 times.9 With inflation currently running above earnings growth, further pressure may push corporate profitability nearer a tipping point. Fortunately, a review of recent earnings calls suggests companies have so far been able to pass price hikes along to consumers. In addition, current S&P 500 profit margins of 12.3% are well above the long-term average.9

Despite slowing earnings growth overall, the dispersion across sectors has been enormous. Energy had an outstanding first quarter, with an expected year-over-year earnings growth rate of 258%, though that number is slightly skewed due to the unusually low earnings base in the first quarter of 2021. At least on the surface, tangible sectors led, including materials (+39%), industrials (+32%), and real estate (+20%), all expected to report earnings growth of at least 20%. On the other hand, both financials (-21%) and consumer discretionary (-34%) are reporting greater than 20% earnings declines.8

Image

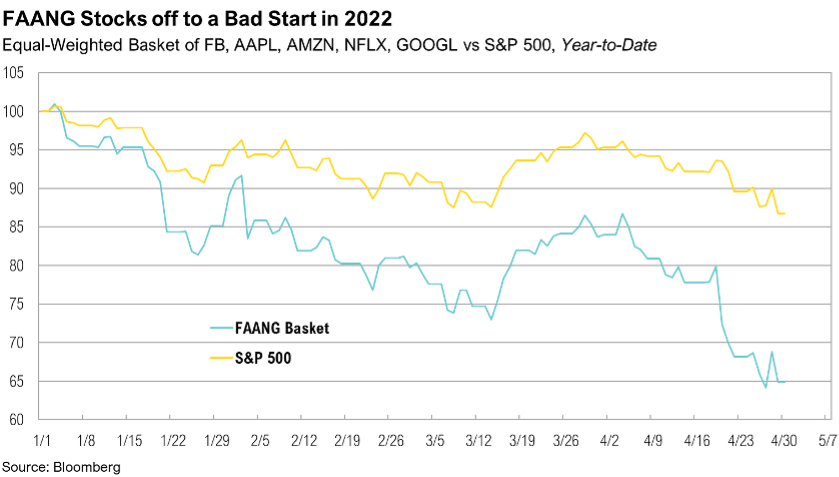

The first quarter was important for the “FAANG” names, given the earnings growth needed to rationalize their above-average valuations. Netflix was the first to report on April 19th, beating analyst earnings per share estimates by 22%.10 However, the stock plummeted over 35% the next day on the news that the company lost 200,000 subscribers, its first decline in paid users since October 2011. Alphabet, Google’s parent company, was next, reporting earnings per share of $24.62, compared to estimates of $25.91, a 5% miss.11 This represented an 8% decline in profit from the fourth quarter of 2021, dragged down by poor YouTube ad revenue, which the company attributed to European advertisers cutting ad spending due to the war in Ukraine. The stock finished down 18% over the month of April. Meta, Facebook’s parent company, beat relatively low analyst expectations by 6%. However, revenues rose just 7% in the quarter, marking the first time in Facebook’s 10-year history as a public company that the firm failed to achieve double-digit revenue growth.12 Amazon reported its first quarterly loss in seven years, after online shopping cooled off as consumers returned to pre-pandemic habits and spent more money in person at stores.13 The stock fell 14% the next day as a result. Apple was the lone bright spot, surprising earnings by 11% and beating analyst revenue estimates for every product category except iPads.14

The disappointing earnings season for the FAANG stocks resulted in their weight in the S&P 500 dropping from 17% on March 31 to 15% at the end of April, and they cumulatively contributed -2.7% to the S&P 500’s -8.7% return in April. If we are indeed at or near a tipping point in the corporate earnings cycle, the performance of the “FAANG” giants will play a pivotal role in anchoring investor sentiment.

Markets

April marked the worst month for the S&P 500 since the onset of the pandemic in March 2020, as the index fell 8.7%. Small caps did even worse, falling 9.9% as measured by the Russell 2000 Index. From a style perspective, value stocks, measured by the Russell 1000 Value Index, outperformed the Russell 1000 Growth Index, dropping 5.7% (versus 12.1%). The 6.4% of outperformance by value stocks over growth stocks marked the largest spread between the two indexes since March 2001, when markets were in the process of unwinding the excesses of the dot-com bubble. From a sector perspective, consumer staples were the only sector with positive returns, up 2.5% over the month, as investors fled to names with more stable earnings and dividends. Energy was the second-best performing sector, down just 1.5%. Historically higher growth sectors were punished over the month, including communication services (-14.1%), consumer discretionary (-11.9%), and technology (-10.9%), all down double digits.

Image

Stocks outside of the U.S. outperformed their U.S. counterparts during the month. Foreign developed market equity returns, as measured by the MSCI EAFE Index, fell 6.4% in U.S. dollar terms. The MSCI Emerging Markets Index fared even better, down 5.6% in U.S. dollar terms. A big reason for international equity outperformance is its lower exposure to technology companies, as the MSCI EAFE and Emerging Markets Indexes have an 8% and 20% weight to the sector respectively, compared to 27% for the S&P 500.

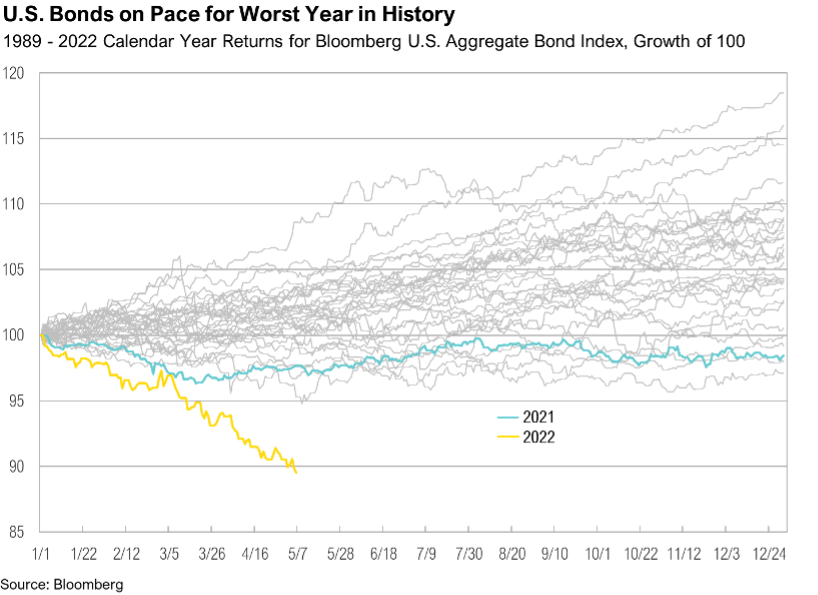

Within fixed income securities, the Bloomberg U.S. Aggregate Bond Index was down 3.8% over the month and is down 9.5% year to date. This significant drop represents the index’s worst year since it was created in 1976, surpassing the previous record of -2.9%, which occurred in 1994. The yield curve rose and steepened over the month. The 10-year yield rose 57 basis points from 2.32% to 2.89%, and the two-year yield rose 42 basis points from 2.28% to 2.70%. As a result, short-term bonds outperformed longer-term bonds, as the Bloomberg U.S. Aggregate 1-3 Year Index fell just 0.6%. High-yield bonds struggled as well over the month, falling 3.6%. Finally, international developed and emerging market bonds finished the month down 7.7% and 5.6%, respectively, as the U.S. dollar strengthened considerably against foreign currencies.

Image

Looking Forward

Persistently high inflation has pushed the U.S. consumer and the overall economy to a tipping point. As we look forward, we will continue to focus our efforts on how consumers and policymakers respond to incoming inflation data. On April 13, president of the St. Louis Fed James Bullard summarized the predicament faced by the Federal Reserve in an interview with the Financial Times:

“It is a fantasy to think the Fed can tame the fastest U.S. inflation in four decades without aggressively raising interest rates… We have to put downward pressure on the component of inflation that we think is persistent.”15

Referring again to the April University of Michigan Consumer Sentiment press release:

“Who would not be apprehensive about future conditions, even if on balance they anticipated a continued expansion? Monetary policy now aims at tempering the strong labor market and trimming wage gains, the only factors that now support optimism… The probability of consumers reaching a tipping point will increasingly depend on prospects for a strong labor market and continued wage gains. The cost of that renewed strength is an accelerating wage-price spiral.”1

Unless inflation moderates meaningfully, the Fed faces an agonizing dilemma, albeit one of its own making. Because it waited so long to address inflation, it now must abruptly slow economic growth and risk a recession in the process. The alternative is equally unattractive. If it fails to do enough, inflation could wreak even more havoc, allowing stagflation to take hold and further eroding what is left of the Fed’s already waning credibility.16

The expectation in the market is that Central Banks around the world will continue with interest rate increases through the rest of 2022. The global economy entered 2022 with good fundamentals and pent-up demand coming out of the COVID-19 pandemic. Robust labor markets and consumers with strong balance sheets remain supportive of an economic recovery, but risks are rising. With headline inflation of 8.3% and the expectation of tighter monetary policy, the Fed’s ability to engineer a “soft landing” of taming inflation without hindering growth remains a key concern for investors.

At RMB, we feel that strong fundamentals and continuation of the economic recovery that started before the Ukraine invasion should help markets over the longer term, but the risks in the short-term are rising. Uncertainty regarding inflation, Fed policy, elevated geopolitical tensions, COVID, and corporate earnings will keep volatility elevated in the near term. We believe that the income component of our clients’ investment portfolios – the interest paid from owning bonds and stock dividends – will be a more important factor of investment returns going forward. To help weather the short-term volatility we are likely to experience in the coming months, we continue to recommend that clients stick to their long-term investment allocation targets and use the market volatility to their benefit by taking advantage of rebalancing opportunities to selectively make changes within their portfolios.

Citations

1. UofM: http://www.sca.isr.umich.edu/

2. Federal Reserve: https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20220504.pdf

3. Morningstar: https://www.morningstar.com/etfs/xtse/vbal/quote

4. BLS: https://fred.stlouisfed.org/series/CES0500000011#0

5. BLS: https://www.bls.gov/news.release/cpi.nr0.htm

6. Federal Reserve Board of Governors: https://fred.stlouisfed.org/series/REVOLSL#0

7. BEA: https://www.bea.gov/data/income-saving/personal-saving-rate

8. Factset: https://insight.factset.com/sp-500-earnings-season-update-april-29-2022

10. CNBC: https://www.cnbc.com/2022/04/19/netflix-nflx-earnings-q1-2022.html

11. NYT: https://www.nytimes.com/2022/04/26/technology/google-alphabet-earnings-profit.html

12. CNBC: https://www.cnbc.com/2022/04/27/meta-fb-q1-2022-earnings.html

13. WSJ: https://www.wsj.com/articles/amazon-amzn-q1-earnings-report-2022-11651110202

14. CNBC: https://www.cnbc.com/2022/01/27/apple-aapl-earnings-q1-2022.html

16. Economist: https://www.economist.com/leaders/2022/04/23/why-the-federal-reserve-has-made-a-historic-mistake-on-inflation

Disclaimers

Performance Disclosures

All market pricing and performance data from Bloomberg, unless otherwise cited. Asset class and sector performance are gross of fees unless otherwise indicated.